EPR Fees in Europe explained: what packaging businesses need to know in 2026 and beyond

How EPR is changing packaging strategy across Europe

It’s a mistake to think of Extended Producer Responsibility (EPR) as just another background compliance issue. As countries across Europe and the world implement packaging reforms, it is fast becoming one of the most powerful commercial levers in packaging design.

Successfully navigating this new landscape requires an understanding of the fragmented picture EPR is creating. While a common principle underpins every version of EPR - producers fund the collection, sorting, and recycling of packaging waste – the reality is far more complex. Fee structures, incentives, and penalties vary significantly by country, creating a patchwork of regulatory environments that packaging decision-makers must actively manage.

At the same time, there is a clear direction of travel in Europe. EPR systems are expected to harmonise as part of the EU’s Packaging and Packaging Waste Regulation (PPWR) by 2030. Until then, businesses are operating in an interim period where understanding national differences is critical to managing both cost and compliance.

This is creating a diverse landscape where some markets are highly evolved, others are still taking shape, and some remain comparatively simple in their approach. As such, we can broadly group nations into three tiers based on the kind of EPR reforms they have implemented. Here, you can learn more about those tiers to support your business growth in Europe for the rest of the decade.

At the same time, there is a clear direction of travel in Europe. EPR systems are expected to harmonise as part of the EU’s Packaging and Packaging Waste Regulation (PPWR) by 2030. Until then, businesses are operating in an interim period where understanding national differences is critical to managing both cost and compliance.

This is creating a diverse landscape where some markets are highly evolved, others are still taking shape, and some remain comparatively simple in their approach. As such, we can broadly group nations into three tiers based on the kind of EPR reforms they have implemented. Here, you can learn more about those tiers to support your business growth in Europe for the rest of the decade.

Share this story

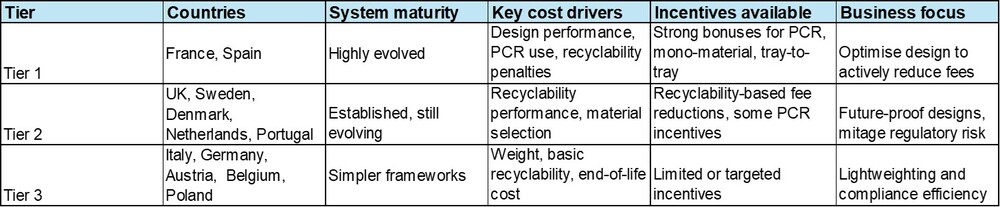

EPR fee modulation across Europe and the UK - at a glance

A high-level comparison of how EPR fee structures differ across major European markets

A high-level comparison of how EPR fee structures differ across major European markets

EPR fee methodologies and incentives vary by country and are subject to change as PPWR implementation progresses.

Tier one: France and Spain - highly evolved systems driving behaviour change

Tier one countries use EPR as an active policy tool to deliberately steer packaging design by financially rewarding circular choices and penalising poor ones.

France sits at the leading edge of EPR fee modulation with systems designed to go beyond cost recovery and actively shape consumer packaging choices, followed by Spain.

France is arguably the most advanced with a model built around a detailed bonus–malus structure which, from 2026, directly rewards or penalises specific design decisions. Financial incentives are tied to the use, quality, and certification of post-consumer recycled (PCR) content which is locally sourced within a 1,500 km sourcing and recycling radius from the geographical centre of mainland France. Alongside significant bonuses for verified PCR content, the system is expected to evolve further from 2028, with enhanced rewards proposed for hard-to-recycle and emerging solutions such as PET tray-to-tray recycling systems.

At the same time, poorly designed packaging is actively discouraged. Materials that disrupt sorting or recycling processes can incur severe penalties, creating a system where design mistakes carry immediate financial consequences. Importantly, the unnecessary use of materials increases fee exposure, reinforcing lightweighting as an essential complementary lever alongside recyclability and recycled content.

In short, France’s approach mirrors a no-claims discount in car insurance – good performance leads to lower fees, while poor performance increases them.

Spain takes a similarly progressive approach, although it uses a slightly different structure. Its system combines multiple incentives, including bonuses for exceeding PCR thresholds and additional rewards for mono-material formats. Crucially, these incentives are cumulative, reinforcing the value of combining recyclability, recycled content and material efficiency.

What defines this top tier is intent. These systems are not passive. They are engineered to accelerate circularity by making the ‘right’ packaging choices financially attractive and the ‘wrong’ ones increasingly expensive. In this context, lightweighting enhances the financial impact of every positive design decision.

What this means for packaging decisions

In these markets, packaging design decisions have a direct and measurable impact on EPR costs. Choices around material structure, recyclability, certified recycled content and unnecessary weight all influence fees. For businesses, success depends on proactively designing packs to meet both technical and regulatory performance criteria, rather than treating compliance as a downstream obligation.

Spain takes a similarly progressive approach, although it uses a slightly different structure. Its system combines multiple incentives, including bonuses for exceeding PCR thresholds and additional rewards for mono-material formats. Crucially, these incentives are cumulative, reinforcing the value of combining recyclability, recycled content and material efficiency.

What defines this top tier is intent. These systems are not passive. They are engineered to accelerate circularity by making the ‘right’ packaging choices financially attractive and the ‘wrong’ ones increasingly expensive. In this context, lightweighting enhances the financial impact of every positive design decision.

What this means for packaging decisions

In these markets, packaging design decisions have a direct and measurable impact on EPR costs. Choices around material structure, recyclability, certified recycled content and unnecessary weight all influence fees. For businesses, success depends on proactively designing packs to meet both technical and regulatory performance criteria, rather than treating compliance as a downstream obligation.

Tier two: UK, Scandinavia, Portugal and the Netherlands - established frameworks still taking shape

Tier two systems are structurally robust but still evolving, creating an environment where early alignment with recyclability and material principles delivers strategic advantage.

The UK, Scandinavia, and the Netherlands represent a second tier of EPR systems. These markets have robust frameworks in place, but key elements are still being refined.

In the UK, the introduction of EPR marks a fundamental, complementary change to the previous Packaging Recovery Note (PRN) system. Packaging contribution fees are now determined using a recyclability-based methodology that assesses the performance of packaging across its lifecycle, from collection through to end-market application. While fee structures are still being finalised, weight remains a central cost driver, making lightweighting one of the most reliable ways to manage exposure despite regulatory uncertainty.

In the UK, the introduction of EPR marks a fundamental, complementary change to the previous Packaging Recovery Note (PRN) system. Packaging contribution fees are now determined using a recyclability-based methodology that assesses the performance of packaging across its lifecycle, from collection through to end-market application. While fee structures are still being finalised, weight remains a central cost driver, making lightweighting one of the most reliable ways to manage exposure despite regulatory uncertainty.

A similar dynamic exists across Scandinavia. Countries such as Sweden and Denmark use tiered systems based on recyclability, with clear financial differences between high- and low-performing packaging designs.

In Sweden, for example, fee modulation is driven primarily by how easily a pack can be recycled, with additional incentives for lightweighting, geometry optimisation, and material simplification.

Denmark uses a colour-coded system, where lower-recyclability formats can attract significantly higher fees than optimised alternatives. Packaging containing materials such as PVC, PVdC, PET‑G, silicone, or rubber‑like substances is treated unfavourably within the modulator framework and is effectively penalised.

The Netherlands combines both approaches. Its system, managed by Verpact, rewards improvements in recyclability while also offering targeted incentives for incorporating recycled content in specific applications. Importantly, it recognises incremental progress, meaning even partial design improvements, including downgauging, can unlock financial benefits.

The hallmark of the second tier is that the direction of travel is clear, even if the detail is still evolving. For businesses, early alignment with recyclability principles and lightweighting can deliver a competitive advantage, even before systems fully mature.

What this means for packaging decisions

While fee structures are still developing, the signal is unmistakeable: packaging that is easy to collect, sort and recycle – and that uses less material - will cost less over time. Businesses should focus on future proofing designs through material simplification, weight reduction and close alignment with recyclability guidance to limit both short-term exposure and reduce the risk of later redesigns.

The hallmark of the second tier is that the direction of travel is clear, even if the detail is still evolving. For businesses, early alignment with recyclability principles and lightweighting can deliver a competitive advantage, even before systems fully mature.

What this means for packaging decisions

While fee structures are still developing, the signal is unmistakeable: packaging that is easy to collect, sort and recycle – and that uses less material - will cost less over time. Businesses should focus on future proofing designs through material simplification, weight reduction and close alignment with recyclability guidance to limit both short-term exposure and reduce the risk of later redesigns.

Tier three: Italy, Germany, Austria, Belgium and Poland - systems that are currently simpler in structure, but evolving

Tier three countries apply simpler, less differentiated EPR frameworks, but still increase cost pressure on packaging that performs poorly at end of life.

Italy, Germany, Austria, Belgium and Poland currently operate more straightforward EPR systems, although this simplicity should not be mistaken for low impact.

In Italy, fees are structured around recyclability bands, with packaging classified according to how effectively it can be sorted and recycled within the existing infrastructure. While there is currently no direct incentive for recycled content, packaging that falls outside established recycling streams faces higher fees. Crucially, most flexible plastics are grouped into broad categories with limited differentiation and treated as non-recyclable for fee-setting purposes. This means downgauging and weight reduction are the main cost-control levers for businesses reliant on flexible materials.

In Italy, fees are structured around recyclability bands, with packaging classified according to how effectively it can be sorted and recycled within the existing infrastructure. While there is currently no direct incentive for recycled content, packaging that falls outside established recycling streams faces higher fees. Crucially, most flexible plastics are grouped into broad categories with limited differentiation and treated as non-recyclable for fee-setting purposes. This means downgauging and weight reduction are the main cost-control levers for businesses reliant on flexible materials.

Austria and Germany follow a similar principle but with increasing alignment to future EU requirements. Mechanisms are already in place to encourage recyclability and the use of recycled materials, supported by broader mechanisms such as the €800 per tonne levy on non-recycled plastic waste.

In Germany, producers must register with the Central Packaging Register (ZSVR) and participate in a licensed dual system, which is responsible for collecting EPR fees and financing the recovery and recycling of packaging waste. In both Austria and Germany, the EU budget contribution of an €800 per tonne levy on non-recycled plastic packaging waste is already having a tangible impact, reinforcing a defined pathway towards recyclability at scale. Importantly, while PET food trays placed on the market are subject to this levy, current legislation actively encourages tray-to-tray recycling to improve real-word recyclability at scale of PET food trays. This presents a strategic opportunity for businesses adopting kp Tray2Tray®, as regulators are increasingly focused on real recycling outcomes.

Weight reduction and basic recyclability remain the primary levers for controlling EPR costs.

Belgium takes a more focused approach, concentrating almost entirely on the real net cost of recycling. Fees are closely linked to how efficiently packaging can be collected, sorted, and recycled, strongly incentivising packaging that minimises material use while performing well at end of life.

Poland is implementing a new EPR scheme for packaging with transitional rules starting from 2026 reaching full, state-controlled operation by 2028.

These systems may be less complex, but they still reinforce a simple, consistent message. Packaging that is heavier and harder to recycle will cost more.

What this means for packaging decisions

In these markets, weight reduction and basic recyclability remain the primary levers for controlling EPR costs. While incentives for recycled content or advanced structures are currently limited, packaging that falls outside established recycling streams will steadily become more expensive. Businesses should prioritise lightweighting, material efficiency and compatibility with existing recycling infrastructures while monitoring future regulatory developments.

Poland is implementing a new EPR scheme for packaging with transitional rules starting from 2026 reaching full, state-controlled operation by 2028.

These systems may be less complex, but they still reinforce a simple, consistent message. Packaging that is heavier and harder to recycle will cost more.

What this means for packaging decisions

In these markets, weight reduction and basic recyclability remain the primary levers for controlling EPR costs. While incentives for recycled content or advanced structures are currently limited, packaging that falls outside established recycling streams will steadily become more expensive. Businesses should prioritise lightweighting, material efficiency and compatibility with existing recycling infrastructures while monitoring future regulatory developments.

From compliance to commercial strategy

Despite the differences between tiers, one common theme runs across every market: EPR fees are fundamentally weight-based and performance-driven.

That has two immediate implications. First, lightweighting delivers universal benefits, reducing costs regardless of geography. Second, design for recyclability is quickly becoming an essential prerequisite for cost control. In this context, materials, formats, and structures must be based on financial decisions as much as technical ones.

As Europe moves towards greater regulatory alignment under PPWR, these national variations will begin to converge. Until that point, success will depend on the ability to navigate a fragmented market, optimise for multiple systems simultaneously, and treat compliance not as a constraint, but as a strategic advantage.

Businesses that perform strongly will do more than just stay compliant. They will use EPR as a lever to reduce cost, improve material efficiency, and future proof their packaging portfolios.

kp supports customers across Europe and the UK with market leading mono material solutions, tray to tray recycling expertise, and packaging designs aligned to evolving EPR fee structures.

Speak to our team to explore how your current packaging performs under European EPR systems - and where targeted design changes could reduce long term fee exposure.

That has two immediate implications. First, lightweighting delivers universal benefits, reducing costs regardless of geography. Second, design for recyclability is quickly becoming an essential prerequisite for cost control. In this context, materials, formats, and structures must be based on financial decisions as much as technical ones.

As Europe moves towards greater regulatory alignment under PPWR, these national variations will begin to converge. Until that point, success will depend on the ability to navigate a fragmented market, optimise for multiple systems simultaneously, and treat compliance not as a constraint, but as a strategic advantage.

Businesses that perform strongly will do more than just stay compliant. They will use EPR as a lever to reduce cost, improve material efficiency, and future proof their packaging portfolios.

kp supports customers across Europe and the UK with market leading mono material solutions, tray to tray recycling expertise, and packaging designs aligned to evolving EPR fee structures.

Speak to our team to explore how your current packaging performs under European EPR systems - and where targeted design changes could reduce long term fee exposure.

Disclaimer

This article is provided for general informational purposes only. Extended Producer Responsibility (EPR) requirements, fee methodologies and incentives vary by country and are subject to change as regulatory frameworks evolve. The information presented does not constitute legal or regulatory advice. Businesses should seek appropriate country specific guidance to ensure compliance with applicable regulations.

This article is provided for general informational purposes only. Extended Producer Responsibility (EPR) requirements, fee methodologies and incentives vary by country and are subject to change as regulatory frameworks evolve. The information presented does not constitute legal or regulatory advice. Businesses should seek appropriate country specific guidance to ensure compliance with applicable regulations.

Useful Links:

- Germany - ZSVR home page

- Austria - Waste Management Act - Federal Ministry of Agriculture and Forestry, Climate and Environmental Protection, Regions and Water Management

- Spain - BOE-A-2022-22690 Real Decreto 1055/2022, de 27 de diciembre, de envases y residuos de envases.

- Sweden - Extended producer responsibility for packaging

- Netherlands - https://www.verpact.nl/en/fee-modulation-plastic

- Denmark - https://mst.dk/media/pavbfqsg/2a-udgave-uk-vejledning-mgb_17112025.pdf

- France - https://www.legifrance.gouv.fr/jorf/id/JORFTEXT000052201296

- Italy - https://www.conai.org/en/businesses/environmental-contribution/plastic-modulated-fee/

- UK - https://www.valpak.co.uk/packaging-waste-recovery-notes-prns-and-extended-producer-responsibility-epr-what-producers-need-to-know/

- UK - Extended producer responsibility for packaging: who is affected and what to do - GOV.UK

- Portugal - Portaria n.º 150/2024/1, de 8 de abril | DR

More like this

Follow us

Contact us

Klöckner Pentaplast GroupCapital House, 4th Floor,

25 Chapel Street

London NW1 5DH

United Kingdom

Legal

Copyright® Klöckner Pentaplast 2026 | kp and other kp marks are registered or proprietary marks of Klöckner Pentaplast